|

1

|

- Marty Blake

- The Prime Group, LLC

- 502-425-7882

|

|

2

|

- Buyer initiated transactions

- Purchases to cover for outages

- Selling what you had

- Balanced book

- Low risk

- Typically transactions with neighbors

|

|

3

|

|

|

4

|

- Large surplus with 33% average reserve margin

- Utilities heavy on baseload and light on peaking

|

|

5

|

- Beginning of real power marketing

- Seller initiated transactions

- Blending of generation sources

- High margins

- Beginning of unbalanced books

- Greater risk

|

|

6

|

|

|

7

|

- June 22-26, 1998 – a week that changed everything

- Prior to June, 1998 the highest price for electric energy was typically

$100/MWh

|

|

8

|

|

|

9

|

- Over 375 traders

- High volume/low margin business

- Unbalanced books

- Higher risk

- Natural gas generation takes off

- Risk management functions

- Reserve margins?

- Coordinated planning?

|

|

10

|

- The California experience

- Insufficient transmission

- Insufficient generation

- Market manipulation

- Seriously making money

- Impact on western markets

- Price caps

|

|

11

|

|

|

12

|

- Bilateral transactions

- Energy markets

- Day ahead market

- Real time market

- Locational marginal price (LMP)

- Financial transmission rights

- Capacity markets

- Ancillary services markets

|

|

13

|

- Nine of the top ten players in the trading market for the third quarter

of last year have now either totally withdrawn or pulled back

substantially from the power trading market. (Power Markets Week, April

14, 2003, p. 26)

- Back to basics for vertically integrated utilities

- Hedge funds and financial institutions enter

|

|

14

|

- Increased counterparty risk

- Increased transmission constraints

- Less liquidity in the bilateral forward power markets

- Increasing and volatile cash demands

- S&P said that it considers purchased power agreements to be

fixed-debt obligations

|

|

15

|

- Incentives to hold reserves have changed

- Capacity markets

- Price volatility in energy markets

- Reserve requirements

- Did large customers get what they wanted when they started this whole

thing?

|

|

16

|

- Provides a market solution for transmission congestion

- Provides a mechanism to deal with energy imbalance

- Provides a commercial market

- What is the future of bilateral trades?

- Role of power marketers?

|

|

17

|

- Historically, transmission congestion was managed using TLRs

- MISO testimony indicated that based on 2003 data, underutilization of

transmission capacity during level 3 and higher TLR events averaged:

- 16.4% in MAPP footprint

- 10.9% in WUMS sub-region

- 7.7% in remainder of MISO

|

|

18

|

- TLRs are an inefficient way to manage transmission congestion

- Energy Markets manage congestion by redispatching generation based on

energy prices at various points in the system (rather than physical

curtailment through TLRs)

- LMP-based market provides a way to compensate generators for redispatch

|

|

19

|

- Real time LMP hourly market that allows self-scheduling

- Day ahead LMP hourly market that allows self-scheduling

- Financial Transmission Rights that hedge against day-ahead congestion

- Capacity assessment and generation commitment for supply adequacy

|

|

20

|

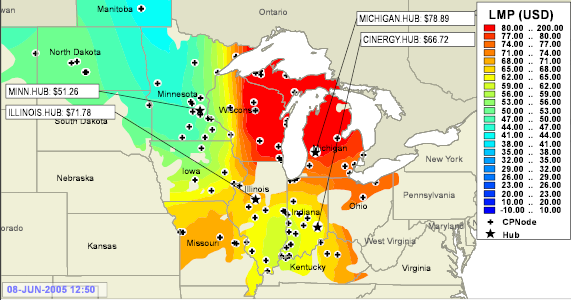

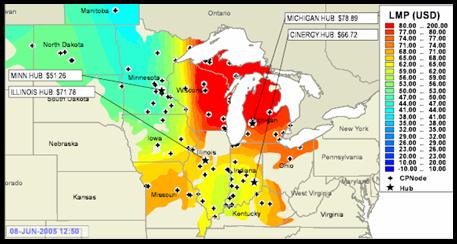

- An energy price that is calculated at each commercial node based on

marginal generation bids for a time period, using a security constrained

economic dispatch

- LMP is a marginal price NOT an average price

- All energy at a commercial node is priced at the LMP

- Congestion between two nodes are valued at the differences between the

nodal LMP’s

|

|

21

|

|

|

22

|

- An FTR is the right to collect the difference in LMP between two

commercial nodes

- Settlement of FTR’s is separate from settlement of energy or congestion

charges

- No schedule is required to collect FTR revenue

- FTR’s can be traded bilaterally or in an auction

|

|

23

|

- An option is a type of FTR in which the owner does not pay congestion

costs when the Target Allocation is negative, but receives congestion

costs when the Target Allocation is positive

- The Target Allocation is equal to the LMP at the Point of Delivery minus

the LMP at the Point of Receipt

|

|

24

|

- Obligations are a type of FTR for which the owner may either pay or

receive congestion costs

- When the Target Allocation is negative, the owner must pay congestion

costs

- When the Target Allocation is positive, the owner receives congestion

costs

|

|

25

|

|

|

26

|

|

|

27

|

|

|

28

|

|

|

29

|

- Market price risk

- Fuel price risk

- Load risk

- Transmission congestion

- Cost of emissions mitigation

- Unit outages and other production management risks

- Counterparty credit risks

|

|

30

|

|

Notes

Notes{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}